Running a successful salon or spa in Nigeria goes beyond just being good with hair, skin, or nails; it involves mastering money management. Between rising operational costs, ever-changing economic conditions, and cutthroat competition, it’s essential to have a solid financial plan in place. Without one, staying afloat can feel like a constant battle, let alone turning a profit.

This guide will provide eight essential financial planning tips specifically tailored to Nigerian beauty and wellness businesses. Whether you’re just starting or have been in the game for years, these strategies will help you avoid common pitfalls, manage your cash flow efficiently, and position your business for steady growth.

Why is financial planning crucial for salons and spas?

Financial planning gives you the clarity to:

- Understand your business’s current financial health.

- Project future income.

- Plan for slow seasons.

- Make smart investments in things like marketing, staff, or new equipment.

Think of financial planning as the roadmap that helps you navigate your business journey. Without it, you’re more likely to end up in a ditch (financially speaking).

8 practical tips for managing your salon or spa finances

Here are eight financial planning tips to help your salon or spa stay profitable in Nigeria:

Tip 1: Master cash flow management

Cash flow is the lifeblood of your business. In simple terms, it’s the money coming in and going out. You need to keep a close eye on it to avoid running into trouble. Positive cash flow means your business brings in more money than it spends.

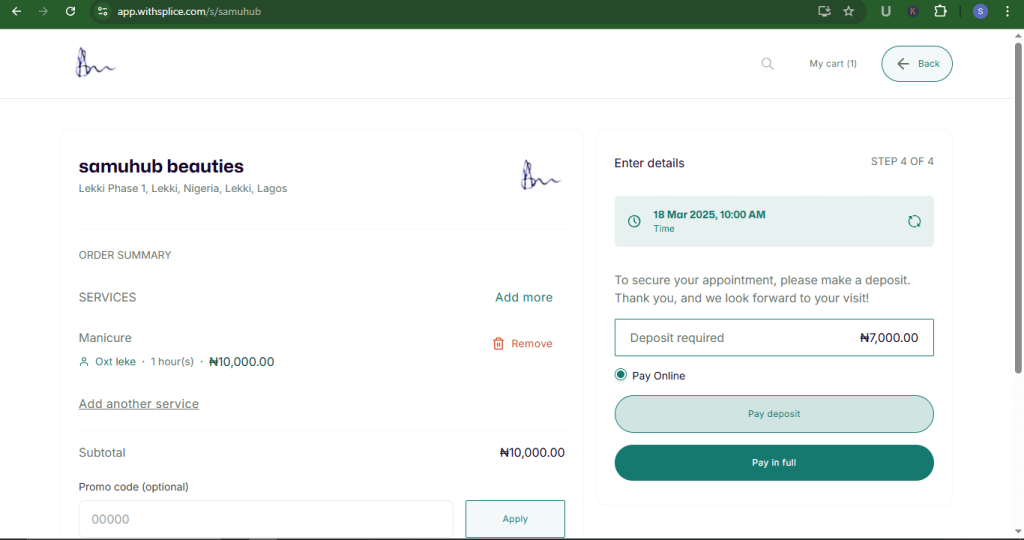

In Nigeria, however, cash flow management can be tricky due to factors like inflation, seasonal demand, fluctuating product prices, and delayed payments. To maintain positive cash flow, streamline your payment process and encourage clients to pay upfront or as quickly as possible.

Splice can help you implement your prepayment strategy.

Pro Tip: Set aside a portion of your earnings for an emergency fund, so you’re not caught off guard by unexpected expenses like equipment repairs or rising product costs.

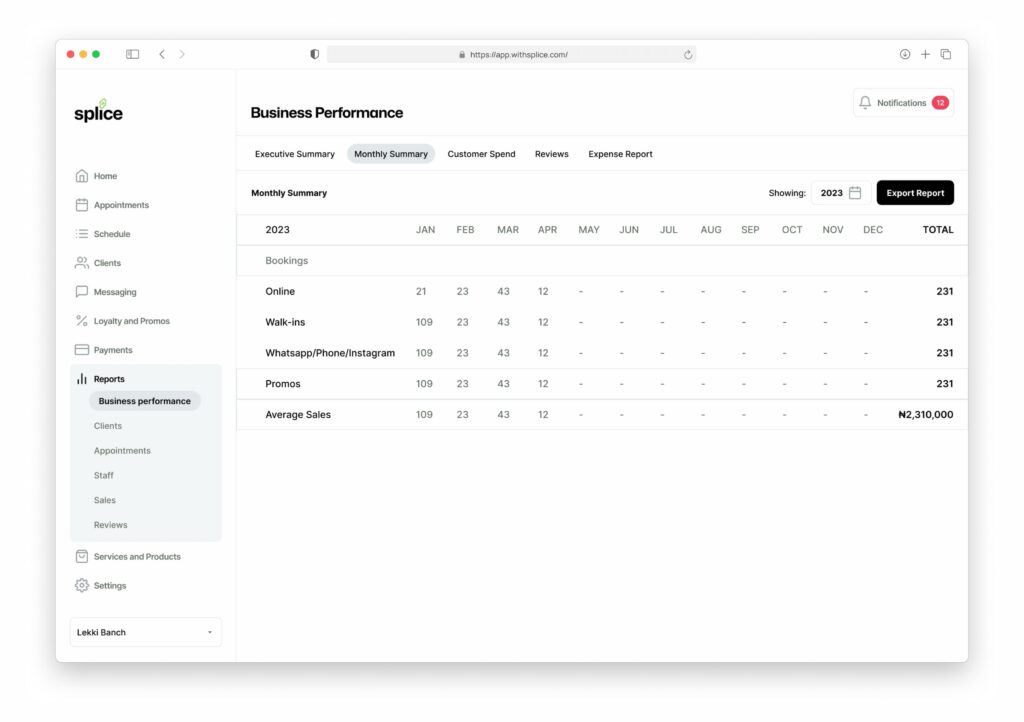

Tip 2: Analyse financial reports regularly

Before you can improve anything, you need to know where you currently stand financially.

Analysing your financial reports should be a regular part of your routine. This means looking at your income and expenses, including everything from service revenue by staff to revenue per appointment and even missed appointments. Knowing these numbers gives you a bird’s-eye view of what’s working and where improvements are needed.

For example:

- Which service brings in the most money?

- Are you losing revenue to frequent cancellations or missed appointments?

- What takes the most money?

Understanding these details can help you make informed decisions and grow your business.

Use tools like Splice to get detailed breakdowns by service or client. The more detailed your insights, the better your financial decisions will be.

Tip 3: Forecast spending for the coming year

As you wrap up the current financial year, it’s a good idea to anticipate what next year will look like.

Will your profits increase?

What new challenges might arise?

Accurate projection helps you allocate funds wisely and avoid nasty surprises.

It’s not just about predicting how much you’ll make; it’s also about planning where to invest your earnings. Whether it’s marketing, hiring new staff, or launching new services, make sure every naira is well accounted for.

Tip 4: Set SMART financial goals

If you don’t know where you’re going, how will you know when you’ve arrived?

Setting financial goals gives you something concrete to aim for. Whether it’s increasing retail sales, boosting service revenue, or introducing a loyalty program, your goals should be Specific, Measurable, Achievable, Relevant, and Time-Bound (SMART).

For example, instead of writing “I’ll hire some more staff next year for my medspa,” say “I’ll hire three staff (one aesthetician and two nurses) by the second quarter of 2025.”

Pro tip: For each goal, create a budget. This way, you can track how much you’re spending and measure your return on investment.

Tip 5: Create (and stick to) a budget

Create a comprehensive budget to keep your money focused on the things that need attention. A solid budget helps you manage daily, weekly, and monthly expenses, ensuring you’re not overspending.

While it’s tempting to splurge on the latest beauty gadgets or treatments, always ask yourself: Will this investment pay off? Your clients want quality service, but it doesn’t mean you should chase every new trend.

Prioritise monthly expenses

Some expenses, such as taxes, rent, utilities, staff salaries, and inventory, can’t be avoided. Make them your top priority to keep your business running smoothly.

Create a routine where you pay your essential bills on the same day every month to avoid late fees or penalties. Once your essential expenses are covered, you can allocate the remaining funds to non-essentials like marketing, staff training, or seasonal promotions.

Pro tip: Time your expenses wisely. For instance, it’s better to launch a big marketing campaign just before your busiest season rather than during a slow period.

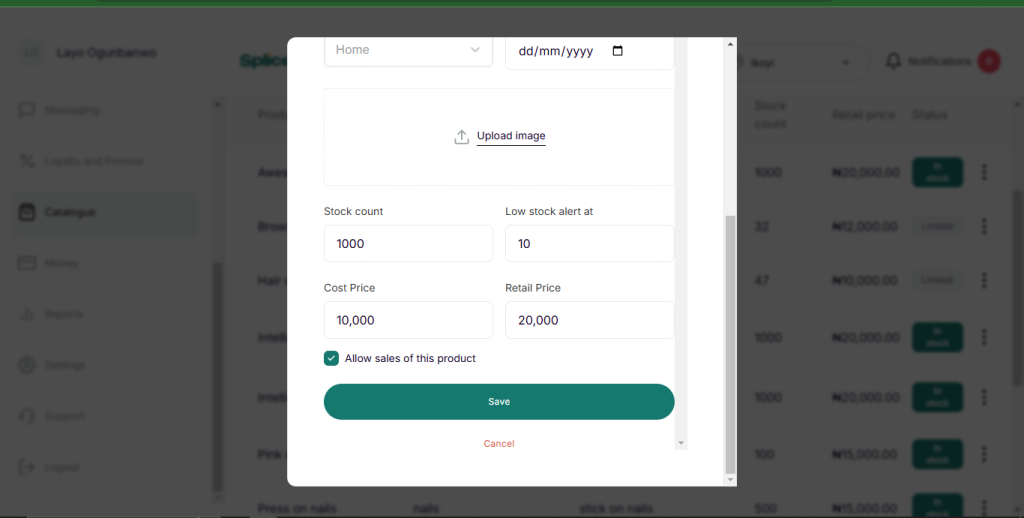

Tip #6: Track inventory

Overstocking ties up cash, while understocking leads to missed sales opportunities. Managing inventory effectively is crucial in Nigeria, where prices fluctuate due to inflation or market forces.

Keep track of your most popular products and services, and stock up accordingly. Buying in bulk when prices are favourable can save you money in the long run, but always make sure the products will sell.

Pro Tip: Invest in an inventory management system to monitor stock levels, predict future needs, and avoid over-purchasing. Splice can help you with this.

Tip #7: Offer multiple payment options

Your clients are more likely to pay promptly when they have convenient payment options. Offering a variety of payment methods (e.g., online payments, mobile transfers, and contactless payments) can significantly increase appointment bookings.

Moreover, using a comprehensive payment processing system can provide real-time insights into your earnings and transaction history, making it easier to monitor your financial health.

Splice software integrates secure payment systems that make it easy for salons and spas to accept several payment methods.

Tip #8: Plan for growth

Growth is the goal, but it often requires additional capital. Whether you want to expand your space, open a new location, or invest in equipment, securing funding is crucial. Start by saving a portion of your profits for your growth plans.

Also, consider applying for loans. In Nigeria, getting a loan for a beauty business can be challenging, but it’s not impossible. SME-friendly banks and microfinance institutions offer tailored loans, and there are government grants for small businesses. Keeping a clean credit history will improve your chances of securing favourable loan terms.

Pro Tip: Before applying for any loan, ensure you have a solid plan for how you’ll use the funds and how you’ll pay them back.

Conclusion

Financial planning is not just a buzzword. It’s the foundation of a successful beauty or wellness business in Nigeria. By applying these eight financial planning tips in your salon or spa, you’ll be well on your way to building a financially stable business that can withstand the ups and downs of the market.

As you grow your beauty business, let Splice be your partner to automate your processes.